The problem with Net Revenue Retention

Net Revenue Retention Rates (NRRs) are the new black. Investors, founders, and CFOs look at NRR to gauge the health of a business. Some even say that if they could only choose one metric to monitor a business, it would be NRR. [1]

The NRR is computed by dividing today’s revenue that was generated by customers who already existed yesterday, by the revenue that this same set of customers generated yesterday:

Revenue in t from customers who already existed in t-1

NDR(t)= ------------------------------------------------------

Revenue in t-1For example, a net dollar retention of 120% in year \(t\) means that the revenue from customers who were already customers in the prior year \(t-1\) increased by 20%. This occurs when the (1) additional revenue that is due to retained customers spending more is greater than (b) the loss of revenues due to some customers churning.

The revenue of a firm with a NRR greater than 100% would grow even if it stopped acquiring new customers. The typical conclusion is that that the firm is successful in making more money out of customers it has already acquired.

However, I have stumbled across a phenomenon that leads to a >100% NRR even though retained customers did not increase their spending. The cause of this phenomenon is what I call the second-year spike.

The “Second-Year Spike”

Consider a firm that acquires 10 customers in each month of year 2020. It acquires 10 customers in January 2020, 10 in Februrary, and so forth. At the end of 2020, it has acquired a total of 12*10=120 customers.

Assume that each acquired customers stays forever and assume that each customer spends \(10€\) per month. We can then compute the revenue the cohort 2020 makes in 2020 as follows:

Revenue of customers acquired in Jan 2020 = 12 * $10 = $120

Revenue of customers acquired in Feb 2020 = 11 * $10 = $110

...

Revenue of customers acquired in Nov 2020 = 2 * $10 = $20

Revenue of customers acquired in Dec 2020 = 1 * $10 = $10and therefore

Total Revenues of cohort 2020 in year 2020

= $120 + $110 + ... + $10

= $660Since customers stay forever churn, the revenue of that same cohort one year later in 2021 is given by:

Total Revenues of cohort 2020 in year 2021

= 120 Customers * 12 Months * $10

= $1200In summary, the cohort 2020 makes $660 in 2020, whereas it makes $1200 in 2021. It looks like customers have increased their spending from one year to the next, doesn’t it?

But if we look closely, the increase from $660 to $1200 is simply because the customers of cohort 2020 were acquired throughout the year. And it happens to be that, for example, customers acquired in December 2020 contributed only 1 month worth of revenues ($10) in year 2020, but 12 months of revenues ($120) in year 2021.

In other words, revenues in the cohort’s second year spike just because the second year is the first year in which all customers of the cohort are observed over a full 12 month period.

Debunking Chewy’s 120% Net Revenue Retention

In their S1 filing, Chewy claims the following:

“Our fiscal year 2018 embedded growth from existing customers (for customers acquired before January 29, 2018) was 120%. In other words, our net sales in fiscal year 2018 would have grown by 20% fiscal year over fiscal year as a result of increased spending among our customer base without any net increase in customers” [2]

In other words, Chewy attributes its 120% net revenue retention rates to its ability to “increase spending” among retained customers. Chewy makes it looks as if retained customers increased their spending by 20%. That interpretation is flawed.

A simple analysis shows that retained customers indeed increase their spending, but by ~4% rather than the suggested 20%. The reason is that the 120% net revenue retention rate is inflated because of the second-year spike.

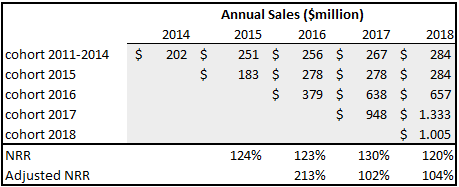

We can see this by looking at Chewy’s cohort data:

The 2018 NRR of 120% can be computed as follows:

\[ NRR_{2018}=\underbrace{(284+284+657+1333)}_{\textrm{Revenue of retained customers in 2018}}/\underbrace{(267+278+638+948)}_{\textrm{Revenue in 2017}}\approx 1.2=120\% \]

But notice that this number is inflated because revenues of cohort 2017 spike from $948 to $1333 (a 40% increase). It is likely that most of this increase is due to the second year spike and has nothing to do with customers increasing their spending.

To come up with a more realistic NRR, we could leave cohort 2017 out of the equation. Below I computed an adjusted NRR based only on cohorts 2011 to 2016: \[ \textrm{Adjusted NRR}_{2018}=\underbrace{(284+284+657)}_{\textrm{Revenues of cohorts }\\ \textrm{2011-2016 in 2018}}/\underbrace{(267+278+638)}_{\textrm{Revenues of cohorts }\\ \textrm{2011-2016 in 2017}}\approx 1.04=104\% \]

Once we control for the second-year spike, net revenue retention drops from 120% to merely 104%. Suddenly the proclaimed “embedded growth” of 20% of the customer base slows down to a marginal 4%, and Chewy looks way less impressive. Would you still invest in the company?

Conclusion

- Investors, Founders, and CFOs look at net revenue retention to gain insights into whether retained customers increase their spending and by how much.

- A high (e.g. 120%) net revenue retention rate does not necessarily mean that the firm is successful in increasing spending among retained customers.

- A high net revenue retention can come from the “second-year spike”. The second-year spike boosts a cohort’s revenues in the its second year simply because that is the first year where all customers of that cohort can contribute to revenue for a full year.

- In a cohort’s first year, customers that are very late to the party (e.g. acquired in December) can only contribute to revenues for a single month.

- Investors must be careful when interpreting net revenue retention rates. Before you interpret the number, you have to (1) carefully look at how the metric is defined, (2) which revenues are considered, and (3) whether the second-year spike is a potential problem.

References

- [1] https://www.youtube.com/watch?v=v3sjDEUJ-mM

- [2] https://www.sec.gov/Archives/edgar/data/1766502/000119312519124430/d665122ds1.htm